Bear Market Emotions: Strategy vs. Reaction

Market volatility is stressful for many investors, and 2022 offered plenty of stress tests. The bear market that began in early January sent stocks on a wild ride with far more downs than ups. The S&P 500 hit its low point for the year in mid-October, down more than 25% from its bull market high. The tech-heavy Nasdaq was hit even harder, falling almost 36%. The indexes were still down by about 20% and 35% respectively at the end of the year.1

Resist Temptation

It can be tempting to sell when faced with falling stock values, but that may not be a wise decision. Stock losses only exist on paper until you sell, so selling at the wrong time might just lock in losses and cause you to miss out on gains when the market turns upward.

On the other hand, it’s not always wise to invest too aggressively when prices are rising. While it’s natural to feel some concern about “missing out,” rushing into a “hot” investment may result in buying at an inflated price that doesn’t reflect the true value of the asset.

Stay the Course

In any market situation, it’s important to make investment decisions based on a consistent strategy rather than emotion. Consider this advice from famed investor and mutual fund industry pioneer John Bogle: “Stay the course. Regardless of what happens in the markets, stick to your investment program. Changing your strategy at the wrong time can be the single most devastating mistake you can make as an investor.”2

This doesn’t mean you should never buy or sell investments. However, the investments you buy and sell should be based on a sound strategy — beginning with a diversified portfolio appropriate for your risk tolerance, financial goals, and time frame. A well-constructed portfolio can help carry you through market ups and downs, but you should also have a clear strategy for how to build your portfolio over time.

Steady as She Goes

One approach that might help steady your nerves is dollar-cost averaging, which involves investing a fixed amount on a regular basis, regardless of share prices and market conditions. Theoretically, when the share price falls, you would purchase more shares for the same fixed investment. This may provide a greater opportunity to benefit when share prices rise and could result in a lower average cost per share over time. Reinvesting any dividends, capital gains, and interest income may also add shares to your portfolio at lower cost.

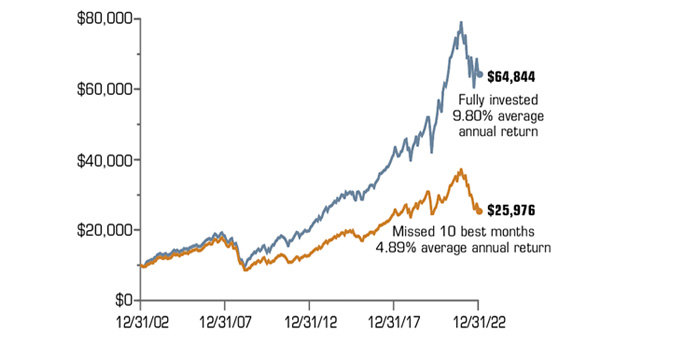

Long-Term Commitment

“Time in the market” is generally more effective than trying to time the market. An investor who remained fully invested in the U.S. stock market over the past 20 years would have received about 2.5 times the return of an investor who missed the best 10 months of market performance. Surprisingly, two of the 10 best months occurred in July and October of 2022.

Growth of $10,000 initial investments

Source: Refinitiv, 2023, S&P 500 Composite Total Return Index for the period 12/31/2002 to 12/31/2022. The S&P 500 is an unmanaged group of securities that is considered to be representative of the U.S. stock market in general. The performance of an unmanaged index is not indicative of the performance of any specific investment. Individuals cannot invest directly in an index. This hypothetical example is used for illustrative purposes only and does not consider the impact of taxes, investment fees, or expenses, which would reduce the performance shown if included. Rates of return will vary over time, particularly for long-term investments. Actual results will vary. Past performance does not guarantee future results.

If you are investing in a workplace retirement plan through regular payroll deductions, you are already practicing dollar-cost averaging. If you want to follow this strategy outside of the workplace, you may be able to set up automatic contributions to an IRA or other investment account. Or you could make manual investments on a regular basis, perhaps choosing a specific day of the month.

Dollar-cost averaging does not ensure a profit or prevent a loss, and it involves continuous investments in securities regardless of fluctuating prices. You should consider your financial ability to continue making purchases during periods of low and high price levels. However, dollar-cost averaging can be an effective way to accumulate shares to help meet long-term goals.

All investing involves risk, including the possible loss of principal, and there is no guarantee that any investment strategy will be successful. Diversification is a method used to help manage investment risk; it does not guarantee a profit or protect against investment loss.